Drop in births after the spread of Covid-19

Since the start of the pandemic in March 2020, a remarkable downward trend in births has been registered all over the world, causing an abrupt baby bust.

This phenomenon had been pointed out by the Brookings Institute that estimated that by June 2020 US births would plunge by 300.000. It is no coincidence that many surveys show how people planning to have babies rapidly changed their mind: in Italy 37% of them abandoned the idea.

This is a dramatic phenomenon and the situation does not seem to be improving: Joshua Wilde’s research at the Max Planck Institute for Demographic Research in Germany shows that it is likely to go on for months. In October he estimated that by February there will have been a 15.2% decline in births, but there is evidence that this trend will extend until August.

The reasons behind this drop are strictly linked to the uncertainty people are going through, both in their personal and professional life. Not surprisingly, some studies demonstrate that a 1% increase in the national unemployment rate corresponds to a 1% drop in birth rate.

A focus on Italy

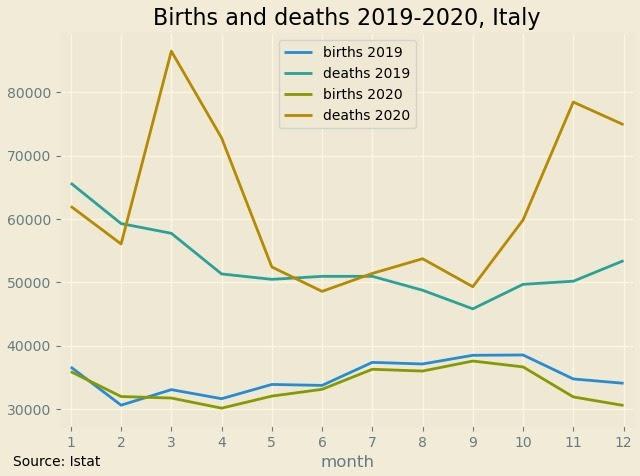

According to Istat, on December 31st 2020 the italian population counted 59.257.566 people, pointing to a decrease of 0.6% compared to the numbers tracked at the beginning of the year. These data result from three factors: a dramatic drop in births, a considerable surge in deaths and a fall in migratory flows.

First of all, the child births recorded in Italy in 2020 are 404.104, 16.000 less than 2019. This amount represents a new negative record since the Unification of Italy.

In addition to this, the number of deaths related to Covid-19 is not negligible. In fact, it amounts to 746.146 (+15.6% compared to the 2015-2019 average), which is the highest level of deaths registered since the Second World War.

Another important reason causing the demographic crisis is the halt in international immigration movements that experienced a considerable decrease of 66.3% during the first wave of the virus, then they slightly recovered during the second one (-18,2%).

Effects on the pension system

The demographic crisis due to Covid-19 could lead pension systems to collapse. In this regard it is important to distinguish between two different types of pension systems actually existing: the funded pension system and the pay-as-you-go system. In the first one, the current generation pays pension contributions which are directly invested in capital markets in a variety of assets such as sovereign bonds, corporate bonds and equity. Then, at the time of retirement, workers will collect an amount equivalent to paid contributions increased by the rate of return of their investment. Clearly, funded systems incorporate a high level of risk, since they are particularly exposed to the financial markets’ performance.

On the other hand, pay-as-you-go systems are the most common and in many countries they carry more than 90% of retirement income. In this case the revenue collected from the current workers is immediately disbursed to the generation of retirees. The formula expressing this concept is the following:

MPt= αWt= αWt-1(1+n)(1+m)

Where:

MPt = pension amount in t

αW=workers contribution

n=population growth rate

m=production growth rate

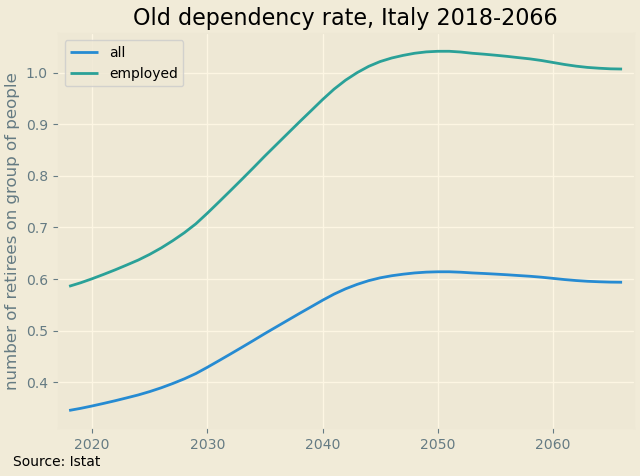

Consequently, it is evident that this kind of pension system could suffer an extreme mismatch between the number of contributors and retired people to whom they have to pay the pension cheque. A useful indicator showing this phenomenon is the old-age dependency ratio, a demographic indicator that measures the size of non-working age groups of the population relative to that of people of working age.

The wide gap between new births and deaths carried by Covid-19 is a real danger in this sense. In fact, if in the future there will be fewer people of working age, as a consequence of the above-mentioned downturn in births, there will be less tax revenue generated to pay for pensions for old people. In the next forty-five years the old-age dependency ratio will increase from 34% to 59% making it harder to sustain the current pensions without applying a labour force boost or a labour tax raise. It is important to note that the dependency ratio is calculated on people of working age, not on all the employed. In order to compute the old-age dependency rate on net contributors (employed) it is necessary to correct the share of population in the working age with the employment ratio. We have decided to use 59% (data related to 2019) as the employment rate, the percentage of people employed in the working age population, but it will not be constant in the next decades.

Furthermore, the old-age dependency ratio is the quotient between people over 65, conventionally the retirees and the working age population. The intention of the ratio is to compare retirees and the workers sustaining their pensions. However, over 65 misrepresented the Italian retirees because the social insurance system, with the major contribution of quota 100, allowed workers to retire earlier. In conclusion, both the ratios should be higher.

Predictions for the future

The Italian population passed its peak in terms of size and it’s likely we will assist toin its decline in the next decades.

A country’s population growth can take place through two channels: a positive difference between births and deaths (natural balance) or immigration. In this regard, in the last 28 years, Italy suffered from a negative natural growth rate which it used to balance with immigration until 2014.

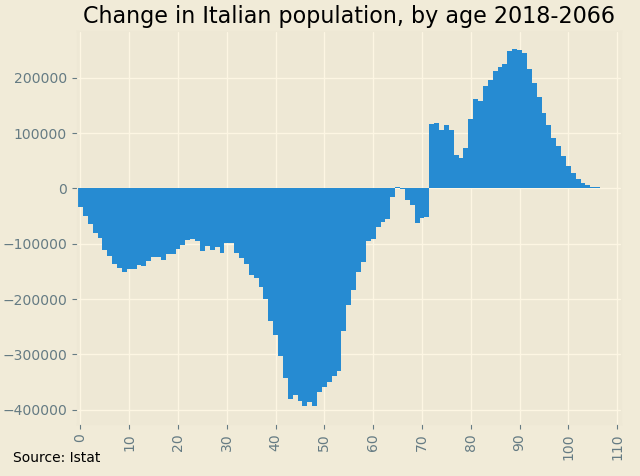

By using Istat and UN’s forecasts to get a view of Italian demographics until 2066, it is possible to observe that Italy will go from the 24th largest country worldwide, in terms of population in 2020, to 42nd in 2060 and 50th by 2100. The expected population in 2100 counts 47.81 million units. This would be a 12 mln reduction in 80 years, with almost 150.000 people less each year, an amount equivalent to the number of people living in Cagliari, Sardinia’s biggest city. This decrease will hit its largest magnitude in 2060, with a projected contraction larger than the number of inhabitants of Venice (250.000+).

On the other hand, it is important to observe that not all the age bands will experience a deterioration in absolute terms.

According to an Istat projection expecting 53.5 mln of people in Italy in 2066, the under 70s will diminish by 11.3 mln and the over 70s will increase by 4.3 mln.

In 2018 people under the age of 70 represented 83,3% of the entire Italian population while this percentage will fall to 73% in 2066. By looking at under 30s we observe that they are around 28.5% in 2018 and they will reach 25.9% in 2066. The most consistent age band will increase from 53 to 57 and the median age will surge from 45.2 to 50.2 in 2066, while life expectancy, now at 83.67, will shoot up at 92.22 in 2090.

An older and less numerous population is going to heavily affect the country’s economy. This is because a higher number of retirees will request a bigger share of public expenses to be allocated to their pensions. This will trigger heavier social security taxes on workers: not surprisingly, by 2043 each one of them will need to contribute for at least a retiree, depressing their net salary. A lower net salary will decrease the incentive to work in the country. At the same time, skilled people will be likely to find employment abroad and the gap between Italian and non Italian net wages will grow.

In addition to this, if the number of workers plummets, due to an aging population, while the wages do not grow, retirees will receive poorer pensions if compared to a fully funded alternative.

Another economically damaging effect due to the demographic crisis is that a reduced number of working people compared to the entire population will delay the GDP per capita growth, since a consistent part of the population will be among the retirees.

On top of that, an aging population will slow GDP growth. It is the consequence of the enormous amount of public expenses intended for retirement accounts. A dollar on pension and a dollar on research or other investments do not drive to the same results.

GDP growth is vital to sustain the sovereign debt, increased at unseen levels with Covid-19 (1).

Furthermore, an increase of the old-age dependency ratio and an older population results in lower real estate prices. The demographic decline has its negative effects especially in rural areas, where the outflow of people is not likely to change.

Needless to say, people’s impossibility to buy houses due to the lower salaries they are going to receive, most of the housing will remain in “old hands”.

Consequently, old people will suffer from the falling values of their houses. (2)

Policies to prevent the collapse

Women’s employment rate is heterogeneous in the Italian peninsula going from 65% in Trentino to 29,4% in Campania (2019), with an average level of 50% and a gap of 18% with men’s.

Increasing women’s employment could reduce the old dependency rate on employees, since the employment rate will grow. On the other hand, the old-age dependency rate on the working age population will not change since this share of population would not see any adjustment.

Immigration, instead, can change both ratios by increasing the working age population since, assuming that they will work in the same proportion as the italian population, the working age population will increase as the employees do. Both will unload the burden of pensions from the current workers redistributing on a larger audience.

There are differences between these two possible policies when it comes to retirement: women (or other unemployed) will perceive a bigger pension than the minimum or the survivor’s pension if they worked, while immigrants will not if they remain in their native country.

On the other hand, the effect of immigrants’ flow to the social insurance system of a country tends to decline when they become net receivers of those services (retirees) and new flows are needed (3). Moreover, immigration provides employment in humble jobs where natives refuse to work.

A comparison with other EU countries

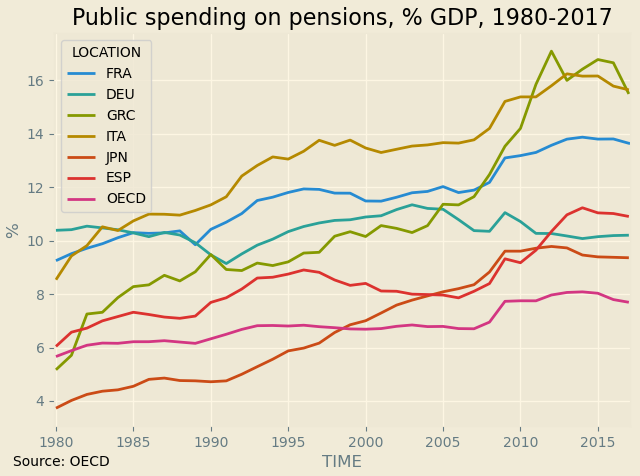

While the “Belpaese” let its pension expenditure expand in the last decades, France and Germany managed to stymie their public pension expenditure, allowing it to grow at a lower rate.

The OECD average shows a large increase in spending after the 2008 crisis, during high unemployment periods when companies tended to encourage early retirement to their older employees instead of laying them off (4).

Older workers with the perspective of unemployment have to choose between the job market, where old age is negatively perceived, and early retirement.

Obviously, after or during a crisis where the labour market demand (employers) is depressed and the supply (future employees) skyrockets, wages are lower than before and early retirement becomes more viable as a solution.

The current situation is not so different: it is likely that Covid-19 will create early retirees as unemployment after the “blocking of layoffs” ends. This event would trigger a jump in social security expenses as in 2008, accelerating the effects of a certain future increase.

Moreover, as a consequence of the future layoffs the old-age dependency ratio will increase driven by the amount of people exiting the employed category to become either retirees or unemployed.

These groups will cause higher expenses that could be paid through heavier taxes on work or additional debt, both solutions would be an excessive burden on actual and future workers’ shoulders.

(1) THE EFFECT OF POPULATION AGING ON ECONOMIC GROWTH, THE LABOR FORCE AND PRODUCTIVITY, Powell, Maestas, Mullen

(2) Aging and Real Estate Prices: Evidence from Japanese and US Regional Data, Saita, Shimizu, Watanabe

(3) Immigration, aging and the regional economy, Park, Ewings 2009.

(4) Ebbinghaus B (2006) Reforming Early Retirement in Europe, Japan and the USA

A CLEF student with an insatiable hunger for knowledge. Very passionate about finance, political economy, social sciences and classical music.

Third year economics and finance. Economics enthusiast. Looking at the world through data