Challenger banks, disruptor banks, neobanks — no matter which name you refer to them by, there’s no denying the debilitating impact these banks have had on the global financial market. Since their inception, challenger banks have revolutionized the banking industry, amassing customers to the point where they represent a credible threat to traditional banks today. But, considering the fact that most are currently in a net loss-generating phase amidst a pandemic, can these innovative banks weather the storm? Is the challenger bank business model even sustainable? And can they truly replace the vital, if generally mistrusted, role played by traditional banks?

The Rise of Challenger Banks

Although they offer many of the same services, challenger banks can be distinguished from traditional banks in that they operate solely online. This allows them to reduce their costs significantly and offer a much more personalized service to customers.

The evolution of challenger banks is grounded, in many ways, in the 2008 financial crisis. After the crisis hit, the general public rapidly lost trust in traditional banking institutions, which provided the opportunity for a new form of banking to rise up. This form of banking seemed especially attractive to the public given the transparency and customer-centric approach championed by these banks, a welcome relief from the approach taken by traditional banks. In Europe particularly, many challenger banks began to pop up due to the deregulation of the financial sector following the crisis, which reduced the barriers to entry that had previously characterized the financial sector. Additionally, rapid advancements in technology were supporting the infrastructure for online banking. Given the public’s dissatisfaction with traditional banks and the general economic climate, it was the perfect moment for challenger banks to make their entrance.

Since then, challenger banks have amassed a significant customer base. In 2019, Fincog estimated that around 150 challenger banks in the world had a collective customer base of 200 million. The Fincog Challenger Bank Index, which tracks 100 of the largest challenger banks around the world every month based on search frequency, registered an increase of 55% per year since 2015.

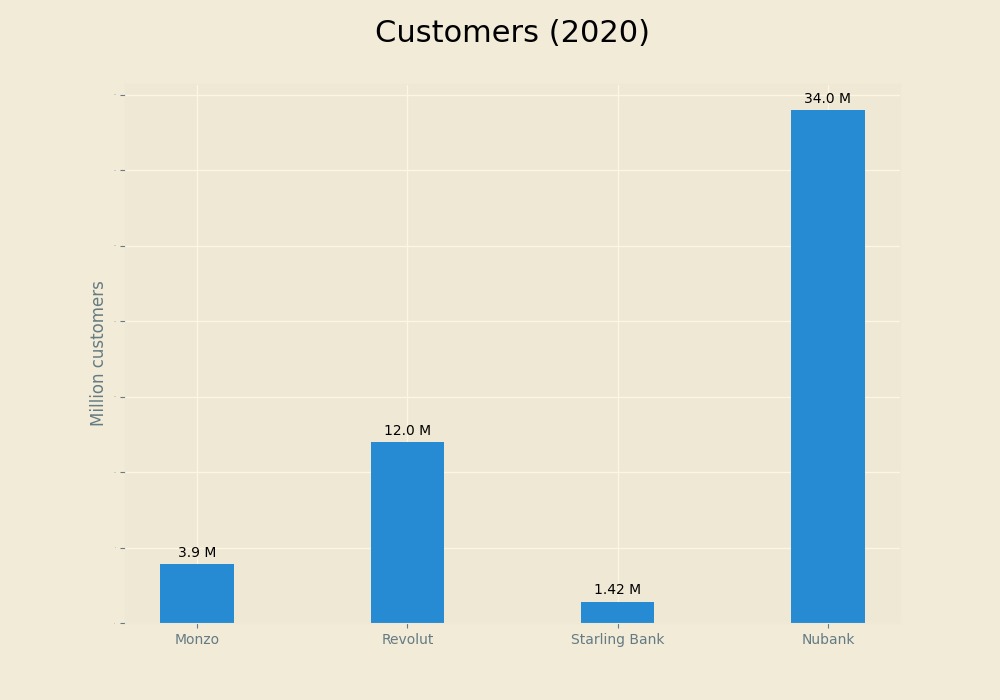

Number of Customers at Major Challenger Banks Around the World

These astonishing numbers boil down to three unbeatable characteristics of challenger banks: ease of use, customer-centricity and competitive pricing. The sheer convenience of managing all their financial operations via their mobile phones drove many people into the arms of challenger banks. Setting up an account with a challenger bank is a notoriously simple process, often taking only 10 to 15 minutes on your phone with little to no human interaction. Additionally, customers value challenger banks’ commitment to transparency and a seamless banking experience. Finally, many of the services offered by challenger banks have no fees attached to them (such as setting up the account, P2P payments, currency exchange etc.) and those that do always display the fees up front.

The Profitability Problem

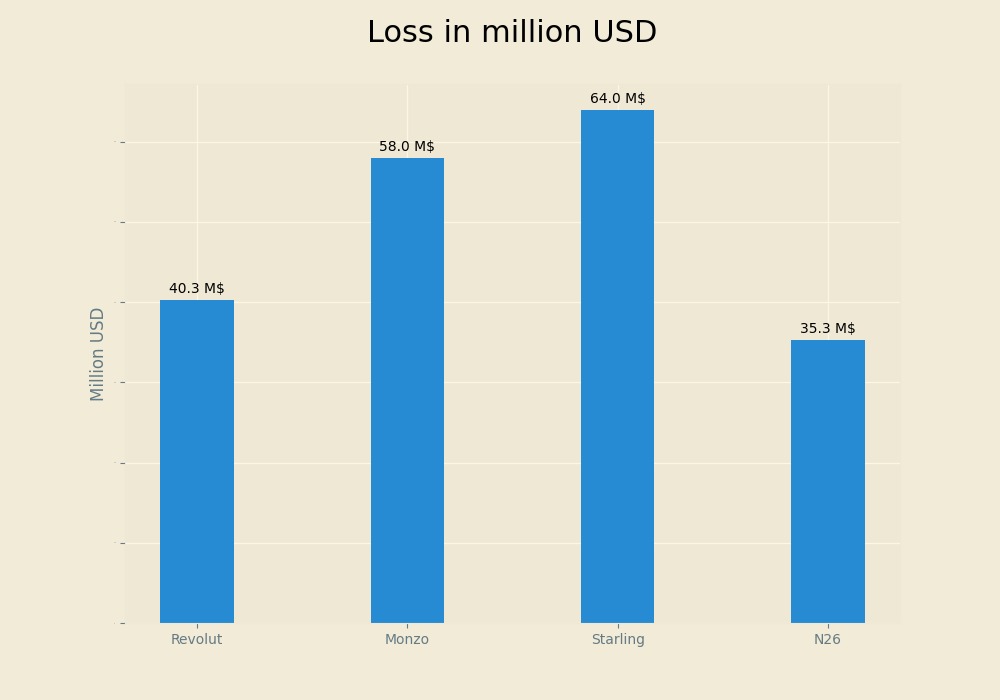

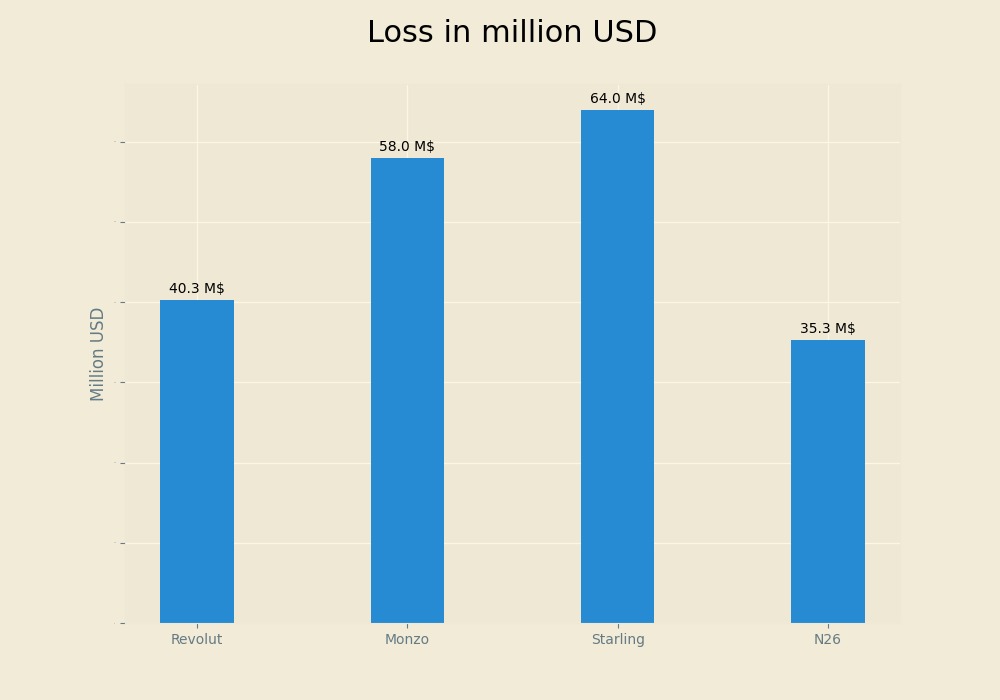

Unfortunately, however, while challenger banks have managed to attract significant popularity, the overwhelming majority have not turned a profit. Even before the pandemic, many challenger banks were struggling to generate profits, as most of these disruptive banks are still in what is referred to as a “net-loss generating phase” and have not yet broken even. The larger the bank, the greater the loss: Monzo, one of the most popular challenger banks with an estimated 3.1 million customers in 2019, for example, registered a loss of $18.71 per customer in 2019.

Additionally, customers are still hesitant to trust these banks with their money. According to research conducted by Accenture in 2020, only around 45% of customers believed that challenger banks would survive to the next year and a fifth said that they would not trust challenger banks with their money.

Net Loss Registered by Different Challenger Banks in 2019

Considering the incredibly competitive pricing, the limited number of banking services and their newborn status in the financial world, however, the fact that most challenger banks have yet to turn a profit should not come as much of a shock. The overwhelming majority of these banks are still in a relatively early phase of their life and so are operating at subscale, offering very few services compared to traditional banks. They require substantial initial investments to build up their brands and to attract customers. Only once they have cleared these initial hurdles and established their foundations with adequate economies of scale, will they be more likely to turn a profit. In fact, the same Accenture study also found that the market share of challenger banks was steadily growing — while 17% of customers had a challenger bank account in 2018, this increased to 23% in 2020.

The Impact of COVID-19

The COVID-19 pandemic has had a drastic, albeit ambiguous, impact on challenger banks. On one hand, overall growth slowed down as consumer confidence in financial institutions fell. In 2018, 6.7% of consumers shifted their primary accounts to challenger banks compared to only 3.8% in 2020. At the same time, however, the pandemic drove up the need for an easily accessible digital bank, encouraging more consumers to open accounts with challenger banks. In the US alone, seven major challenger banks saw their cumulative customer base grow from 28 million users in 2019 to 39 million in September 2020, with industry leader Chime hitting the 12 million mark in February 2021.

As a result, different challenger banks tended to fare differently, depending largely on their structure and the services they offered. Regular challenger banks such as Monzo, N26 and Revolut that are centred around ‘daily banking’, meaning a payment account and money management services, generally experienced a stagnation or even negative growth as customers cut back on spending and credit card use. On the other hand, challenger banks with a greater focus on cryptocurrencies and trading, such as Robinhood, experienced an overwhelming positive impact as first-time investors flooded the market to take advantage of seemingly low stock prices. Additionally, Starling Bank performed incredibly well because of its focus on lending, both to consumers and to small-to-medium enterprises. While consumer lending declined as a result of the pandemic, SME lending saw a massive surge and Starling Bank was able to capitalize on this after being accredited as a Coronavirus Business Interruption Loan Scheme and a Bounce Bank Loan Scheme lender, schemes introduced by the British government to support businesses during the pandemic.

The Impact of COVID-19 on the Growth Rates of Different Challenger Banks

Ultimately, the pandemic may have helped prove what was previously uncertain — that the challenger banks model can be profitable. In October 2020, Starling Bank reported that it generated a profit of £800,000 for the month, becoming one of the first challenger banks to do so.

What Does the Future Hold?

While there’s no denying that challenger banks are here to stay, that does not necessarily mean that they will completely take over the role played by traditional banks. For one, traditional banks provide many services that challenger banks do not, such as mortgages and loans. Additionally, customers are a long way from trusting challenger banks to completely manage all their financial needs. Even those who are customers of challenger banks often use it in conjunction with a traditional bank account and not as their primary bank account. Banks like Chime are still dependent on traditional banks to issue credit cards. Only 3 of the top 10 challenger banks possess a banking license, which enables them to offer the full suite of financial services available at a traditional bank. The rest are, in a sense, not real banks but simply fintech applications that cannot fully take over the role of a traditional bank.

One particularly interesting study found that 41% of millennials would consider taking out a mortgage using an app. Among the top-cited reasons were greater speed, the ease of using an app, the chances of getting a better deal and the convenience of arranging a mortgage at any time. Not surprisingly, therefore, the trend towards using challenger banks as primary accounts is driven by consumer desires’ to have more convenient, transparent and fair financial dealings over which they have greater control. If challenger banks do manage to extend their range of financial services, particularly with regard to loans and mortgage packages, traditional banks could be reduced to mere backend utility providers — still part of the financial world due to their size but no longer the dominant players.

The one significant advantage that challenger banks do have over traditional banks is their ability to adapt and innovate quicker than their counterparts and delve into new markets. In a post pandemic world with increased consumer spending, a sustainable agenda, and a long-term plan to build highly personalized customer experiences, they are likely to thrive. As long as challenger banks place a greater emphasis on profitability and becoming sustainable businesses in their own right, they could carve a permanent position in the fintech world.

Sources:

https://fincog.nl/blog/15/the-profitability-challenge-for-challenger-banks

https://www.accenture.com/us-en/insights/banking/consumer-study-making-digital-banking-more-human

https://fincog.nl/blog/18/performance-of-neo-banks-in-times-of-covid-19

https://www.fintechmagazine.com/banking/will-challenger-banks-lead-post-covid-recovery

https://www.bankingexchange.com/retail-banking/item/8535-us-challengers-grow-users-to-39m-in-2020

I'm a third-year student in the BIG program from Lahore, Pakistan. I enjoy learning about and discussing politics, history, and religion, and particularly the interactions between the three.